Las Vegas homeowners are booking the highest profit margins in years when selling their property, but amid flat prices, those gains have largely leveled off, a new report shows.

Owners who sold their home in March booked an average gain of 23 percent, or $36,000, above their purchase price, according to RealtyTrac. The profit margin was the highest locally since October 2007, when sellers booked an average 31 percent gain.

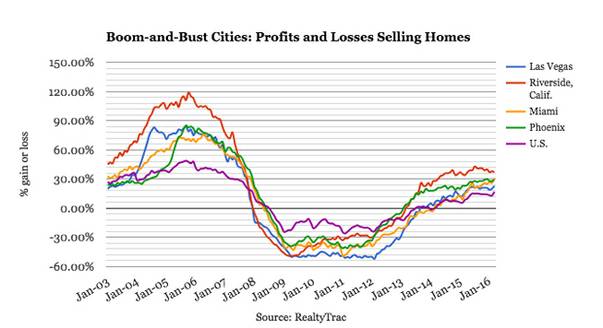

Las Vegas had one of the biggest real estate bubbles in the country last decade, but when the economy crashed, it was one of the hardest-hit markets in the nation. On average, Las Vegas-area home sellers booked a loss every month from January 2008 through August 2013, RealtyTrac data show.

Profit margins have steadily climbed since then but have hovered around 21 percent since May 2015 as sales prices flattened out.

According to the Greater Las Vegas Association of Realtors, the median sales price of previously owned single-family homes — the bulk of Las Vegas’ market — has hovered around $220,000 since June.

After last decade’s boom and bust, sales prices shot up at some of the fastest rates nationally, as investors bought cheap homes in bulk to turn into rentals. Price-growth has slowed considerably the past few years as investors backed out.

Despite the slowdown, Las Vegas sellers are booking higher profit margins than homeowners nationally.

Across the U.S. last month, sellers posted an average gain of 17 percent, or $30,500, according to RealtyTrac. That was the highest margin nationally since December 2007.

Southern Nevada, however, lags behind some other boom-and-bust regions.

Last month, Phoenix-area sellers had a profit margin of 29 percent; Miami, 31 percent; and Riverside, Calif., 37 percent, RealtyTrac reported.