House hunters know all too well that new homes cost more than used ones.

But in Las Vegas, the sticker shock is especially harsh.

The spread in prices between new homes and resales is much bigger in Southern Nevada than it is nationally. The gap has fluctuated in recent years, but overall, buyers pay a far bigger markup for new digs in Las Vegas than they do in other cities.

The gap is wider than historical averages, and developers have to drum up new marketing pitches touting the advantages of a new yet more expensive house to lure buyers amid much-lower prices on the resale market, said Dennis Smith, founder of Las Vegas-based Home Builders Research.

“It’s a pain in the rear-end for the builders,” he said.

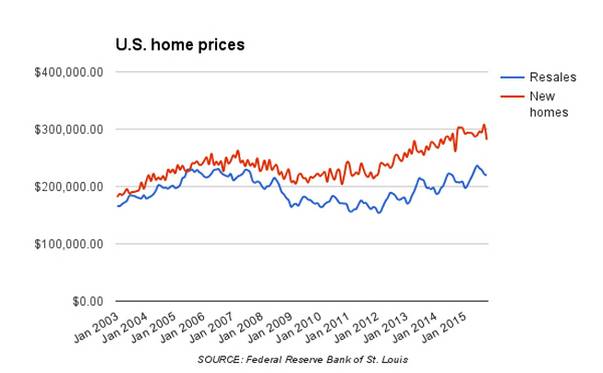

Nationally, new homes sold for a median $281,500 in October. That was 28 percent, or $61,900, higher than the median sales price of previously owned homes that month, according to data from the Federal Reserve Bank of St. Louis.

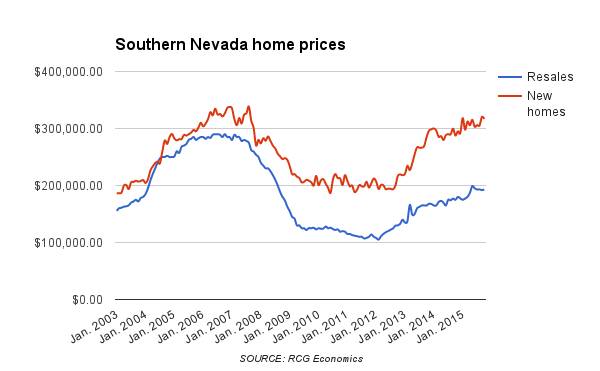

Locally, the median sales price of new homes in October was $316,825. That was 64 percent, or $123,825, higher than the median price of resales, according to data provided by RCG Economics.

Historically, the gap has hovered around 10 to 15 percent, real estate pros say. It widened after the economy tanked but narrowed a few years ago as investors gobbled up cheap homes in bulk, pushing up home prices at one of the fastest rates nationally.

In the last two years, however, as investors backed out and price-growth slowed, the spread has been wider, RCG data show.

There has always been a price-gap between new and used homes, but it's “not as dramatic as you’re seeing now,” RCG founder John Restrepo said.

“When somebody's got an option to buy the same square footage and you have that big of a gap — a new home generally has a lot more to offer than a resale, but that gap needs to be narrower," homebuilder Don Boettcher, Nevada division president for Century Communities, recently told the Sun.

Las Vegas’ gap is “an outlier” among U.S. cities and indicates that local builders are focused on larger, more expensive homes and that the valley’s resale market, once choked by foreclosures, remains in a “recovery phase,” said Lawrence Yun, chief economist for the National Association of Realtors.

The median sales price of previously owned single-family homes is up 9 percent year-over-year but has been largely flat since June, at around $220,000. Sales totals of used single-family homes this year through November are up almost 6 percent from the same time last year but down 7 percent from that 11-month period in 2013, according to data from the Greater Las Vegas Association of Realtors.

A look at Las Vegas home prices over the past 10 years

Personal finances nationwide, especially in boom-and-bust Las Vegas, were wrecked by the recession. Today, amid low credit scores and slow-to-no-growth in many people’s wages, the valley’s housing market is dominated by resales.

Roughly 28,200 used single-family homes sold this year through November, according to the GLVAR, compared to 5,440 new homes this year through October, says Home Builders Research.

Builders don’t cater to everyone, though. New-home buyers typically have the cash for a down-payment, as well as healthy income levels and good credit, said David Crowe, chief economist for the National Association of Home Builders.

New homes also are bigger than ever, which means they’re more expensive, he said.

“They’re a select group of people in the market,” he said of buyers, “and they want what they’d normally be buying, which is a larger, more elaborate home.”

But, he noted, in cities where prices still are depressed from the housing bust, “it’s harder to sell a new home.”

Las Vegas’ market is more stable than it was at the depths of the recession. But business isn’t nearly as robust as it was last decade, during the hyper-inflated bubble years, and plenty of weak spots remain.

Resale prices for single-family homes, for instance, peaked in mid-2006 at a median $315,000 and hit bottom in early 2012 at $118,000. Builders sold nearly 39,000 new homes here in 2005 alone — then just 3,900 in 2011.

Meanwhile, 22 percent of local homeowners with mortgages are underwater, meaning their mortgage debt outweighs their home’s value. That’s down from a peak of 71 percent in early 2012 but still highest among large U.S. metro areas, according to Zillow.

Despite the ups and downs — and the wide price gap — there will always be people who want a new house, just as drivers often prefer a new car, Realty One Group broker Kathryn Bovard said.

“They don’t want the headache; they don’t want the maintenance; they want that new-car feel,” she said.